The ethical and societal implications of blockchain technology and its potential impact on governance and society as a whole.

Search for a command to run...

Thanks for sharing this depth of knowledge.

x402 is a new payment standard that enables micro payments on the web by leveraging blockchain technology. It leverages the existing 402 Payment Required status code to require payment before serving a response and uses crypto-native payments for spe...

The so called AI slop all over the internet is getting less sloppy. NBC News We're living through an extraordinary moment in history. The rapid evolution of generative AI has unleashed an unprecedented creative boom. These tools have democratized co...

In these last few years, layer two blockchains (L2) have become central to Ethereum's scaling efforts. L2s are fast, cheap, and inherit Ethereum's strong security guarantees. Ethereum serves as the settlement layer, and L2s serve as the execution lay...

A blockchain is a peer-to-peer (P2P) network of nodes that maintains a shared ledger. Every node communicates with other nodes in the network using specialized P2P protocols to verify blocks, transactions, store state, etc. When you’re building an ap...

Tokens represent money-like assets, utility (such as governance or access), rewards and points, game items, tickets, and more. Most tokens on Solana follow the SPL token standard or Token-2022 with extensions, which define how tokens are created, tra...

Recently, I posted on my LinkedIn page about the importance of blockchain education and received a lot of questions from people asking me to explain what blockchain technology is. This shows that many people are still unfamiliar with blockchains or have not heard of them, despite their digital literacy. As much as we may want to blame them for not paying enough attention online, it is not fair to blame these people. Instead, we should blame those in the industry who have made it appear as though only highly technical people can understand and participate in the space. This is not the case, and it's important to educate more people about the reality of blockchains.

Blockchains are for everyone, but understanding how to use them in everyday life is necessary to grasp this revolutionary innovation's significance. This is why I am writing this article, to help you understand the concept of blockchain technology, its relevance to you, and its impact on society.

If you made it down here, I am sure you have decided to read through; I welcome you onboard. However, before we discuss the implications and impacts, I would not want to assume everyone knows what a blockchain is. As such, I will start with a brief explanation of it, where we are coming from, and where we are.

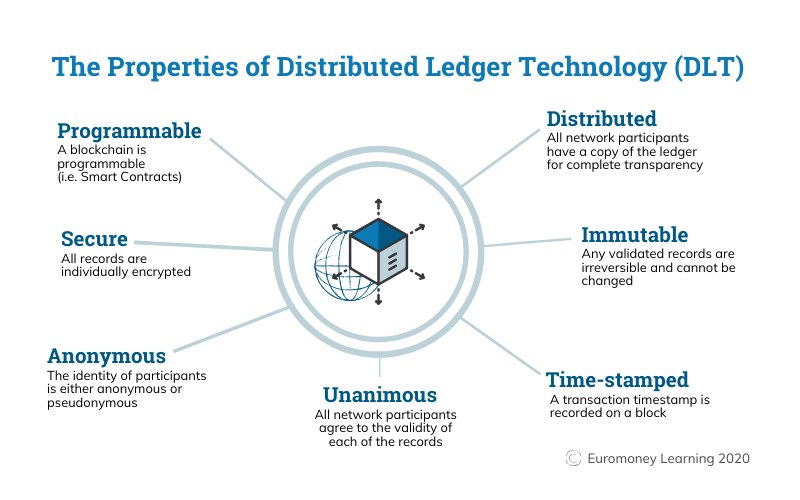

Blockchains are digital ledger systems that allow for secure, decentralized, and tamper-proof record-keeping of transactions. They store information across a network of computers, and each block in the chain contains multiple transactions. So, every time a new transaction occurs, it is recorded on all participants' ledgers, making it highly secure and eliminating the need for a third-party intermediary. It is a continuously growing list of ordered records linked using cryptography and contains a timestamp, cryptographic hash of the previous block, and transaction data.

It is important to note that blockchains are not cryptocurrencies; neither are they an innovation.

Now, let's talk a bit about history. However, most people believe that blockchains' history started in 1991 when two scientists by the name of Stuart Haber and W. Scott Stornetta wanted to create a fully functional system where users could not alter document timestamps (Meaning you would not be able to backdate a document or manipulate it in any form). However, it dates back to 1982 when David Chaum, a cryptographer, first presented his dissertation titled "Computer Systems Established, Maintained, and Trusted by Mutually Suspicious Groups". This was the foundation for the knowledge Stuart Haber and W. Scott Stornetta built on.

By 1992, David Bayer joined the two scientists in incorporating Merkle tree (or Hash Tree) into the design. The definition or explanation of a Merkle tree may sound like a lot, but you don't need to know the key details; just know that it introduced an efficient verification process and an added layer of security, as any tampering with the data in the block would be immediately apparent due to changes in the hash values stored in the Merkle tree. By introducing the Merkle tree, there was a reduction in the amount of data that had to be transmitted, stored, and processed, which made blockchains more scalable.

The concept then evolved through several innovators, from Wei Dai, Hal Finney, Nick Szabo, and Adam Back to Satoshi Nakamoto (pseudonym), who proposed the concept of blockchain as a decentralized and distributed ledger in the Bitcoin whitepaper in 2008. It was implemented as the backbone of the Bitcoin network, and since then, the use cases for blockchain technology have expanded to include many other industries.

You will agree that blockchains have a long evolution history, and we are still early.

I almost got carried away writing about the history of Blockchain technology and how the technology has evolved. Still, I had to pinch and remind myself that it's not a historical novel or a dull old research paper. Well, that is that.

Now back to the ethical and societal implications of this revolutionary technology. To fully dive into each, I will take them as individual sub-topics. First, we discuss the ethical and societal implications and, then, the potential impact of blockchains on governance and society.

This refers to the considerations arising from the impact of blockchains. Since its first use in cryptocurrency, blockchains have brought to light several long-standing ethical, societal, and governmental issues previously thought impossible to address. The bar has been raised, and the technology's impact has resulted in significant changes across several areas. These implications cover many aspects and can include privacy, security, and decentralization, amongst others.

To help you understand the different implications better, I will be discussing them below:

Transparency:

One of the most remarkable properties of blockchains is transparency because it allows transactions to be traceable. We can employ this feature in various fields to increase transparency and accountability and reduce corruption. One such example is supply chain management. By using a blockchain system, each step in the supply chain can be recorded and tracked, allowing for greater transparency and visibility. This is particularly useful in the agriculture industry, where consumers desire to know where their food comes from. Another application of this technology is in voting systems. We can use blockchains to create tamper-proof digital voting systems, enabling transparent and verifiable election results. Additionally, blockchains in the real estate industry can make property ownership records more transparent, making it easier to track the history of a property and ensure that all transactions are accurately recorded.

Anonymity and privacy:

Blockchains have the potential to significantly enhance privacy and security, particularly in light of the growing concerns about data breaches and privacy violations on the web. With the emergence of Web2 platforms, privacy has become a critical issue for many individuals, and blockchain technology offers a powerful solution for protecting personal information and ensuring anonymity.

An example of how blockchains can protect privacy is in the healthcare industry. By using blockchain to store patient medical records, individuals can control access to their information. They can share it with healthcare providers when necessary while ensuring that their personal information is not shared with third parties. Similarly, we can use blockchains to establish decentralized marketplaces for anonymous and secure transactions, providing a safe space for individuals to buy and sell goods and services without revealing their identities. Additionally, blockchains can be applied to create decentralized social networking platforms where users can communicate and share information anonymously without fear of censorship or retaliation.

The examples are just a few ways these can apply to different industries.

Impact on financial systems and the potential for financial inclusion:

We can use blockchains to create several decentralized structures that allow individuals to access financial services, such as small loans, without the need for traditional financial institutions and help to increase financial inclusion for those who may not have access to conventional banking services. These services can be secure and efficient remittance services that allow individuals to send money to family and friends in other countries without intermediaries. This reduces the cost of remittances and increases access to financial services for individuals in developing countries.

As someone who has experienced high bank charges when sending money abroad, I am thrilled to see how blockchains have made global transactions seamless and cost-effective through cryptocurrency. Growing up, my elder sister studied in Europe while we lived in Africa, and I saw firsthand the prohibitive costs of international money transfers. However, now, as a writer for foreign companies, I can receive payments with minimal fees thanks to cryptocurrency. This makes global transactions easy and eliminates the need for excessive third-party interference.

Another way blockchains impacts the financial system is through decentralized finance platforms that allow businesses to access financing and other financial services without the need for traditional financial institutions, increasing financial inclusion for small and medium-sized businesses that may not have access to traditional banking services.

Smart contracts and their potential impact on all walks of life:

Smart contracts are self-executing digital contracts stored and replicated on a blockchain network. They are terms of the agreement between parties written directly into lines of code, and when certain conditions are met, the smart contract automatically executes. Additionally, smart contracts are stored on a blockchain network; therefore, they are transparent, secure, and tamper-proof, making them useful for various industries and applications.

An illustration of the use of smart contracts is in the buying and selling of property. It automates and streamlines the process by executing the transaction and transferring ownership and funds once all conditions are met. In Supply chain management, businesses can use smart contracts to track inventory, manage logistics, and automatically execute payments based on predefined conditions. Also, Insurance companies can use smart contracts to automate the claims process for insurance policies, where policyholders can submit claims on a blockchain platform, and the smart contract can automatically verify the claim and process the payment. Additionally, governments can use smart contracts to automate the delivery of government services, such as issuing licenses and permits, and automatically execute tax and fee charges. Last but not least, we can use smart contracts in human resources to automate the management of employee benefits and compensation, where employers can use smart contracts to manage employee records, manage benefits, and automatically execute payments for salaries and bonuses.

Impact on the economy and job market:

Blockchains brought about a new wave of incredible job opportunities just a few years ago. As technology continues to evolve, we will likely see more job opportunities arise soon. For example, the emergence of the metaverse and NFTs has led to the creation of new job roles, such as metaverse art directors, metaverse architects, and NFT creators. Similarly, the growth of decentralized finance (DeFi) has led to the creation of new roles, such as DeFi analysts, DeFi market makers, and DeFi traders.

Other job opportunities created by blockchains include blockchain developers, consultants, traders, analysts, and community moderators for blockchain-based platforms such as Discord. These jobs offer new opportunities for people to explore and significantly impact the economy and the job market. Blockchains have opened up new avenues for innovation and efficiency and have created numerous job opportunities for people with different skill sets.

Blockchains are driving an economic and job market revolution, and it's exciting to see how they will continue to shape the future of work. The possibilities are endless, and it's an exciting time to be a part of this industry.

Impact on democracy and political systems:

While mentioning almost every point earlier discussed, I have touched a bit on governance. The influence of blockchains on governance is far-reaching, and it can significantly improve the quality of our political systems.

For instance, blockchains can provide secure, transparent, and tamper-proof voting systems that guarantee every vote is counted and the results are not manipulated. This can increase voter turnout and public confidence in the electoral process, especially in countries like Nigeria(where I am from), where voter apathy is high due to a lack of trust in the voting system.

Another critical benefit of blockchains in governance is accessibility. By using blockchain-based systems, governments can create decentralized platforms that enable citizens to access government services and information without intermediaries. This can reduce costs and increase efficiency for government institutions.

Furthermore, we can use blockchains to create decentralized platforms for decision-making and governance. This can enhance citizens' participation in the political process and result in more democratic and transparent governance systems. Overall, blockchain technology has the potential to revolutionize governance and political strategies by improving transparency, accessibility, and security.

Finally, you made it to the end. I had to remove some of the points I wanted to discuss to keep the article concise and easy to understand.

By reading this article, you have gained a comprehensive understanding of the various applications of blockchain technology and its impact on society. Throughout the article, I have discussed the different properties of blockchains, such as decentralization, security, and transparency, and how we can apply them in various industries. I have also explained how blockchain technology can impact governance and political systems by providing a more secure, transparent, and accessible way of conducting activities.

Blockchains have the potential to revolutionize the way we live, work, and interact with one another. From improving transparency and security in voting systems to creating new opportunities in e-commerce and finance, blockchain technology can change how we conduct business, make transactions, and manage our personal data.

As this technology continues to evolve, we must stay informed and adapt to the changes it brings. With this knowledge, we can better understand how we can use blockchains to improve our lives and create new opportunities for growth and development.